You're probably looking at two loan offers right now that refuse to compare cleanly.

One shows a lower rate, but the repayment window is tight and the payment feels aggressive. The other looks more manageable month to month, but the paperwork mentions fees, collateral, and conditions that make your stomach tighten. If you're buying a practice, replacing imaging equipment, or covering a cash flow squeeze, that confusion isn't a side issue. It's the whole game.

Most veterinarians make the same mistake. They focus on the advertised rate first and everything else second. That's backwards. A loan is not just a rate. It's a package of interest, term, fees, flexibility, and risk. The right question isn't “Which loan has the lowest number on page one?” The right question is “Which loan gives my practice the lowest total cost for the outcome I need?”

That's how you compare veterinary practice loan rates like an owner, not like a rushed borrower.

Navigating the Maze of Veterinary Loan Offers

A veterinarian I'd consider typical in this market gets two offers for the same project.

Offer one comes from a bank-style lender. The headline rate looks attractive. The catch is a shorter repayment schedule, more pressure on monthly cash flow, and a closing process full of line items that don't fit neatly into the rate discussion. Offer two has a higher stated rate, but the structure is more forgiving. Payments are easier to absorb, and the loan may fit the clinic's real operating rhythm better.

That's where most owners stall. They're trying to compare a price tag with a cash flow plan, and those aren't the same thing.

The cheapest-looking loan often stops looking cheap once you account for fees, repayment speed, and what the payment does to your operating cushion.

Veterinary medicine has its own financing reality. Your practice isn't a generic storefront. You carry payroll, inventory, equipment needs, seasonal shifts, and client payment variability. A loan that works on paper can still strain the business if it ignores those moving parts.

The fix is simple in concept and harder in practice. Stop looking at offers as isolated rates. Start looking at them as full capital structures. That means asking:

- What is the loan for: acquisition, equipment, build-out, or short-term operating support?

- How long will the asset or need last: years, months, or permanently?

- What does the monthly payment do to my margin: does it preserve room for staff, inventory, and surprises?

- What extra costs sit outside the rate: fees, collateral demands, and payoff restrictions?

A good loan should solve a business problem without creating a new one. If the payment is too tight, the rate doesn't save you. If the term is too short, the “better deal” can choke working capital. If the fees are heavy, the low APR can become a distraction.

That's why smart borrowers calculate total cost first and judge the rate second.

The Four Main Types of Veterinary Practice Loans

A veterinarian buying a clinic, replacing an X-ray unit, and covering a short payroll squeeze should not shop for one generic loan. Those are three different capital problems. Use the wrong structure and your total cost of capital climbs fast, even if the advertised rate looks fine.

The right question is simple: what job is this money doing, and how long should you still be paying for it?

Practice acquisition loans

Use an acquisition loan to buy an existing clinic, buy out a partner, or fund an expansion through another location. This debt should match a long-life asset that produces cash flow for years, so the term needs to support that reality.

The rate matters, but the full structure matters more. A lower rate paired with a short amortization can create a payment that puts pressure on staffing, inventory, and owner compensation. A slightly higher rate with a longer repayment schedule can produce a lower monthly burden and a better real-world outcome.

For acquisitions, compare offers using total cost of capital in two ways. First, calculate the all-in dollars paid over the expected hold period. Second, calculate the monthly payment pressure in year one. If one loan saves interest but leaves the practice cash-starved, it is not the better deal.

Equipment financing

Use equipment financing for assets with a clear useful life, such as imaging, dental, surgical, lab, or software-related hardware. This is usually the cleanest match because the asset supports production over time and often serves as collateral.

Good equipment debt should line up with the income the equipment helps generate. If a new unit improves case capture, speeds workflow, or replaces outside lab costs, the payment should be supported by that gain. If the payment outruns the benefit, the rate is not your main problem. The structure is.

Do not use general operating debt for a long-life equipment purchase unless you have no better option. Keep short-term liquidity available for short-term needs. If you need a separate solution for cash flow support, review working capital financing for veterinary practices.

SBA loans

SBA loans are often the best fit for first-time buyers and for deals that need lower equity injection and longer repayment terms. They work especially well for acquisitions where preserving cash matters more than closing at top speed.

Their value is not just the note rate. Their value is the structure. Longer terms can reduce monthly payment strain, which changes debt service coverage, owner flexibility, and the practice's operating cushion. That is a direct total-cost-of-capital issue, because a loan that protects cash flow can prevent far more expensive mistakes later, such as underfunding payroll, delaying inventory purchases, or relying on high-cost short-term debt.

My advice is straightforward. If you are buying your first practice, review SBA options early, not as a backup plan.

Working capital lines and short-term loans

Use these for payroll timing gaps, inventory buys, marketing pushes, seasonal dips, and temporary operating needs. These products solve timing problems. They should not carry the weight of a multi-year investment.

Borrowers can easily run into trouble. Though a line of credit may seem flexible and a short-term loan quick, both can become expensive if balances are rolled too long or used to fund equipment, build-outs, or acquisition costs. The stated rate is only part of the bill. You also need to measure draw fees, renewal fees, repayment speed, and the risk that frequent payments squeeze your cash position.

Short-term capital has a place. It just needs discipline.

Here's the practical comparison:

| Loan Type | Best Use | What to Watch | Total Cost of Capital Check |

|---|---|---|---|

| Practice acquisition loan | Buy a clinic, partner buy-in, add a location | Amortization, fees, prepayment terms, required liquidity | Compare all-in dollars paid and first-year payment burden |

| Equipment financing | Imaging, surgical, lab, and tech assets | Term length versus useful life, down payment, documentation fees | Match repayment to the years the equipment earns revenue |

| SBA loan | Acquisition financing with lower upfront cash and longer terms | Guaranty fees, paperwork, timing, collateral requirements | Measure payment relief against total fees and lifetime interest |

| Working capital line or term loan | Payroll, inventory, seasonal gaps, short operating needs | Draw fees, renewal costs, repayment frequency, rollover risk | Price the convenience against how fast cash leaves the practice |

Key Factors That Determine Your Loan Rate

Two veterinarians can apply for the same loan amount in the same month and get very different offers. The lender is pricing the full risk of the deal, and your job is to understand which parts of that risk you can improve before you sign anything.

The mistake I see most often is focusing only on the advertised rate. A lower rate with heavy fees, a short repayment schedule, or a large required cash injection can cost more than a slightly higher rate with better structure. Measure the Total Cost of Capital. That means interest, fees, required equity, payment timing, and any prepayment penalty.

Credit quality

Personal credit is still the first filter. It affects whether you qualify, how much documentation the lender demands, and how much cushion they build into the pricing.

A stronger credit profile usually leads to more options and cleaner terms. A weaker profile often shows up as a higher rate, more restrictive covenants, a shorter term, or all three. The practical takeaway is simple. Clean up reporting errors, pay down revolving balances, and avoid new debt before you apply.

Credit also changes your Total Cost of Capital in ways borrowers miss. If weaker credit pushes you into a shorter amortization, your monthly payment rises. That can pressure working capital even if the stated rate does not look dramatically different.

Practice cash flow and loan purpose

Lenders care about one question above all others. Can this practice make the payment comfortably and keep operating without strain?

They look at collections, doctor production, EBITDA, deposit consistency, and how believable your projections are. A practice with steady cash flow gets better pricing because repayment risk is lower. A practice with thin margins, declining revenue, or sloppy financials gives the lender a reason to price defensively.

Purpose matters just as much. Buying a stable clinic, refinancing debt, funding a remodel, and covering payroll are four different credit stories. Revenue-producing uses of capital usually get better treatment than vague requests for general business needs. If the request is tied to equipment, review equipment financing for veterinary practices instead of stuffing the purchase into a broad term loan that may cost more over its life.

Here is the clean way to judge this factor:

- Strong, consistent cash flow supports lower pricing and better terms.

- A clear use of funds tied to revenue or efficiency improves lender confidence.

- A request driven by financial stress or urgency usually costs more and gives you fewer negotiating points.

Term length, collateral, and equity

These three factors shape the actual cost of the loan more than borrowers expect.

A longer term lowers the monthly payment, which can protect your operating account, but it often increases total dollars paid over time. A shorter term may reduce lifetime interest, yet it can strain cash flow if the payment lands too hard each month. You need the term to match the useful life of the asset and the practice's actual cash generation, not your optimism.

Collateral and equity change the lender's downside. More borrower cash in the deal and stronger collateral support usually improve the offer because the lender is taking less risk. That can mean a lower rate, reduced fees, or better repayment flexibility.

Look at these pieces together. Cash flow determines payment capacity. Collateral affects lender protection. Equity shows commitment and reduces reliance on debt. Those inputs shape both the rate and the Total Cost of Capital, which is the number that should drive your decision.

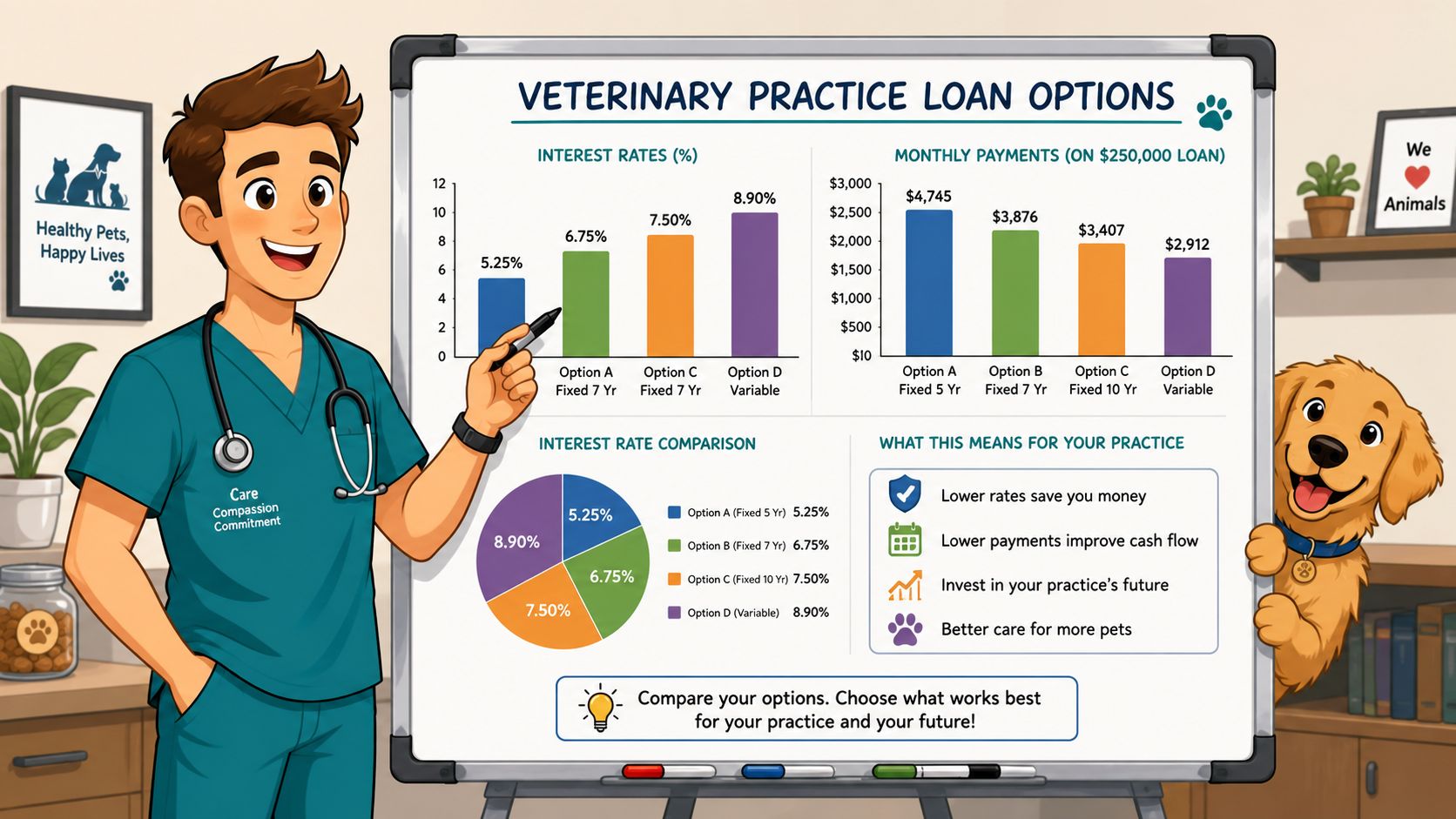

Sample Veterinary Loan Rates and Payment Examples

A buyer signs a practice loan at a rate that looks acceptable on paper. Then the first payment hits the operating account, payroll clears two days later, and the deal suddenly feels expensive. That is why rate shopping alone is sloppy underwriting on your side. You need to measure payment, fees, and term together.

Acquisition financing example

Start with a practice purchase, as borrowers often make their biggest pricing mistake there. They fixate on the quoted rate and ignore the full borrowing structure.

A realistic comparison for veterinary practice acquisition loans starts with four numbers: loan amount, term, monthly payment, and total dollars paid over the life of the note. Add any origination fee, closing cost, and prepayment restriction to that review. Now you are looking at the actual cost of capital instead of an advertisement.

Here is the practical difference. Two acquisition offers can look close on rate and still produce very different outcomes. One may carry a lower payment because the term is stretched out, but the total interest bill is higher. Another may save interest over the life of the loan, yet force a payment that crowds your staffing, inventory, and owner distribution decisions every month.

That tradeoff needs to be deliberate.

Equipment and operating examples

Equipment financing should be judged by the income the equipment supports and by how long the asset will stay useful in the practice. A new imaging unit, dental platform, or in-house lab system can justify financing if the payment fits the revenue lift or efficiency gain. If the repayment period runs too long, you can still be paying for equipment after it stops pulling its weight.

Working capital requires even tighter discipline. Short-term money carries more pressure because the payment starts working against your cash position right away. Use it for short-term needs such as smoothing payroll timing, buying inventory, or covering a temporary gap. Do not use it to fund a long-lived asset or a major ownership transaction. That mismatch usually creates the highest Total Cost of Capital in the file.

How to read an example without fooling yourself

Skip generic payment examples. Use one framework every time:

- Write down the full loan amount

- Confirm the exact repayment term and monthly payment

- List every lender fee and closing charge

- Check for prepayment limits or penalty language

- Compare the payment to your clinic's realistic monthly cash flow

- Calculate total dollars repaid over the life of the loan

A loan offer's true affordability becomes clear when you compare the payment to payroll, rent, inventory, tax obligations, and your minimum operating cushion.

That is the standard I recommend to every veterinary owner. A loan can look cheap in isolation and still be the wrong decision once you place it inside the budget of the practice.

How to Compare Offers Beyond the Interest Rate

This is the part most borrowers skip, and it's the part that matters most.

I call it Total Cost of Capital. You don't need a finance degree to use it. You just need discipline. The goal is to compare two offers on an apples-to-apples basis by combining all borrower costs into one decision framework.

The Total Cost of Capital framework

Use this simple formula:

Total Cost of Capital = total interest paid + upfront fees and closing costs + required carry costs + prepayment restrictions or penalty cost

That's the key number you're hiring the loan to deliver.

A lower advertised rate can still produce a worse outcome if the lender loads the deal with fees, shortens the term so sharply that cash flow gets squeezed, or boxes you into a penalty if you refinance early. If you're weighing ownership financing, it helps to compare structures built for veterinary practice acquisition loans rather than trying to force every offer into the same mental bucket.

Three cost centers borrowers overlook

Most mistakes happen in one of these areas:

- Upfront fees: Origination costs, closing charges, filing costs, and documentation expenses can raise your effective borrowing cost.

- Term mismatch: A shorter term may reduce total interest but create a monthly payment your clinic shouldn't carry.

- Prepayment language: If there's a penalty for paying off the loan early, your flexibility has a price.

The headline rate is only one line item. Owners who ignore the others often choose the wrong loan for the right project.

A practical comparison worksheet

Put every offer into the same worksheet and force each lender into the same boxes:

| Comparison Item | Offer A | Offer B |

|---|---|---|

| Stated APR | ||

| Loan term | ||

| Monthly payment | ||

| Upfront fees | ||

| Collateral required | ||

| Prepayment restrictions | ||

| Fit for the actual purpose | ||

| Effect on monthly operating cushion |

Then ask the question that matters: if revenue softens for a stretch, which loan still lets you sleep?

That's the one you should respect.

Actionable Steps to Secure a Better Loan Rate

Borrowers lose their advantage long before they submit an application. They lose it in the months beforehand by staying disorganized, carrying avoidable credit issues, and walking into underwriting with a vague story.

Clean up the file before the lender sees it

Start with the basics that lenders notice first.

- Review your credit carefully: Fix reporting errors, pay attention to revolving balances, and avoid applying for unrelated debt while you're preparing for financing.

- Organize practice financials: Have clean profit and loss statements, tax returns, production detail, and deposit history ready to go.

- Build a real business case: Show how the loan supports revenue, efficiency, or stability. “Growth” is not a business case. A clear operating plan is.

A lender is asking one question the whole time. Why should I believe this borrower will manage this debt well?

Strengthen the structure, not just the story

Good applicants don't rely on charm. They reduce uncertainty.

That means saving for a stronger down payment when possible, documenting how the clinic handles staffing and inventory pressures, and showing that you understand your own numbers. If cash flow has a weak period, address it directly and explain what changed.

This short video is a useful prompt for that prep work.

Negotiate like an owner

Don't ask only for “the best rate.” Ask for the best full structure.

Try this checklist before you move forward:

- Request a full fee summary: Don't accept partial disclosure.

- Ask about payoff flexibility: You may want to refinance or accelerate later.

- Test the payment against a conservative month: Not your best month.

- Compare more than one structure: Fixed payment comfort matters.

- Challenge mismatched terms: Long-life assets deserve aligned repayment.

Borrowers get better deals when they show lenders two things at once: financial readiness and operational discipline.

Prepared borrowers don't just improve approval odds. They improve negotiating position.

Your Partner in Practice Financing

Veterinary practice loan rates matter, but the rate alone won't tell you whether a loan is smart.

The right way to evaluate financing is straightforward. Choose the right loan type for the purpose. Understand what drives your pricing. Measure the monthly payment against the actual operating life of the clinic. Then calculate total cost of capital so you're not fooled by a pretty headline rate attached to an expensive structure.

That approach protects you in every stage of ownership. It helps when you're buying your first clinic, replacing major equipment, smoothing cash flow, or expanding into a second location. It also keeps you from making the most common mistake in veterinary finance, which is choosing debt based on the first number you see instead of the full cost you will carry.

Specialized guidance matters here because veterinary practices don't behave like generic small businesses. Your revenue timing, staffing pressure, medical equipment needs, and client payment realities create a financing picture that general advice often misses. A lender or advisor who understands those rhythms can help you sort through options faster and with fewer expensive mistakes.

If you want clarity, don't ask only what the rate is. Ask what the debt will cost, how the structure fits your clinic, and what flexibility you'll still have after closing.

If you're sorting through acquisition, equipment, expansion, or working capital options, Veterinary Practice Loans can help you compare structures clearly and focus on total cost, not just the advertised rate.